Having a cash flow model can help you make well-informed decisions about your retirement, not to mention give you the confidence to retire.

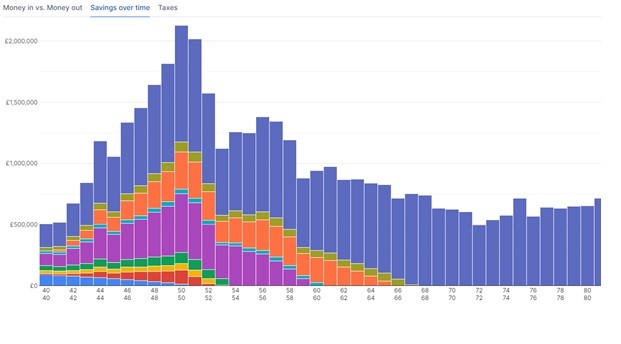

Below is an example of what a cash flow model looks like. We can change parameters such as current assets, mortgage balances, and suggested investment returns (which we tailor to your own risk profile). While the model is dependant on a number of assumptions, it can help you plan when you might be able to retire, the level income that could be achieved and if that income is likely to be maintained throughout your life.

How much will I need to retire?

When speaking to people about retirement, some people say, “I will never retire” or, “you need at least £1 million to retire”. In reality, retirement is a lot closer than most realise, especially if you put a plan in place and see it through. As a rule of thumb, you should be able to take 4% annual income from your pension pot and it last at least 30 years. This is known as the 4% Rule and is the work of William Bengen, a well-respected retired financial adviser. In other words, take the income you need in retirement and multiply it by 25 to give you a target investment pot. The Retirement Living Standards suggest a couple will need £22,400 a year to achieve the minimum standards of living in retirement. This means they would need almost £500,000.

For example, a 30-year-old couple with no savings could each invest £60 per week. To put that figure into context it’s approximately 10% of the weekly UK average salary (£642). If we invest that money and receive the historic average annual return of the global stock market, which is 9%, the £500,000 target would be achievable in 24 years.

Some might say that’s a long time period, which it is, but the couple who had not saved a penny during their twenties could retire at the age of 54. If they started when they were 25 they could retire before their 50th birthdays.

As another example, a married couple has £100,000 in savings and can invest £400 per month each. Using the same assumptions, this couple could grow their wealth to £500,000 within 12 years.

Every person and every family's situation is different. Some require more income than others, some are flexible on their retirement age and others are not. Above are just high-level examples of what is possible from the power of regular investing and compound interest. In reality, an assessment of spending habits, attitude to risk profiling and annual review meetings are essential in ensuring clients achieve their long-term goals.

Cost of retirement

Expenses for people in retirement tend to be lower than during their working lives. There’s less commuting, no need to buy work attire, and you have more time to food shop and make your own meals. In addition, the State Pension can supplement your income once you reach the appropriate age. There is also no requirement to fully retire all in one go. If you don’t like your current job, you might want to ‘retire’ 10 years earlier and work part-time in a business that you find interesting.

The possibilities and options are endless. There’s no need to feel confused or worried about retirement. Cash flow modelling can bring you that peace of mind and confidence by helping you look at all the scenarios available to you, and picking the one that will bring yourself and your family the most joy.

If you would like to view a cash flow model personal to your own circumstances, perhaps work out the age that you could retire or understand how much income you might be able to take in retirement please get in touch. Contact Nick on 01768 222080 or email nick.birtle@armstrongwatson.co.uk.