State pension is valuable but don’t solely rely on it in retirement

Amanda Heys

Financial Planning Consultant

The main state pensions have risen faster than inflation but these state benefits are still low compared with even average earnings.

The new state pension (for those who reached state pension age (SPA) after 5 April 2016) is £179.60 a week and the old (basic) state pension (for those who reached SPA earlier) will be £137.60 a week. Both increases are 2.5%, a rate secured by the so-called ‘triple lock’, which requires these pensions to rise by the greater of:

- the increase in average earnings;

- the rise in prices measured by the consumer price index (CPI); and

- 2.5%.

Other state pensions, such as the state second pension, rise in line with the CPI, meaning a 0.5% increase from April this year.

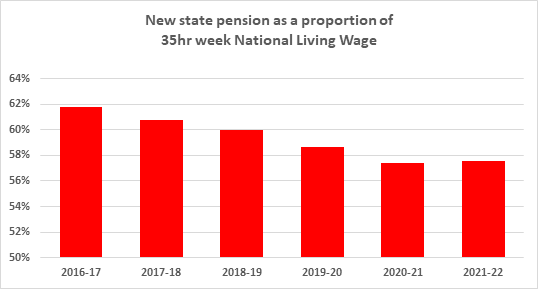

The 2.5% increase underlines the value of the triple lock, which this year delivers state pension recipients an increase of 2% above inflation. The new state pension and National Living Wage (NLW) both came into effect in April 2016, but 2021 will be the first year that the pension has been the faster growing of the two (by 0.3%), although this does little to narrow the significant gap between them.

Compare the positions of Jack, aged 64 and Jill, aged 66. In 2021/22, Jack works a 35-hour week for the National Living Wage of £311.85. Jill, at the new SPA of 66, will receive the new state pension of £179.60 a week – less than 60% of Jack’s earnings. The question is, why has the government set the new state pension so far below the National Living Wage for a full-time worker? The answer is cost. The Government pays the state pension, but it is employers (admittedly including the Government) who have to fund the wages.

According to research from the Organisation for Economic Co-operation and Development (OECD), the UK sits at the bottom of the state pension league table for OECD members – although the new state pension is higher than its predecessor. This lowly position explains why the Government has placed so much emphasis on automatic enrolment in workplace pensions since 2012. Similarly, it demonstrates the need for additional private pension provision regardless of any increase to the state pension.

How much is enough in retirement?

The Retirement Living Standards, based on independent research by Loughborough University, have been developed to help us to picture what kind of lifestyle we could have in retirement. It shows what retirement could look like at three different levels – Minimum, Moderate and Comfortable – and what goods and services would cost for each level.

This can be found at www.retirementlivingstandards.org.uk.

A single person will need about £10,200 a year to achieve the minimum living standard, £20,200 a year for moderate, and £33,000 a year for a comfortable lifestyle. For couples, it is £15,700, £29,100 and £47,500 respectively.

-

A ‘minimum’ lifestyle covers all your needs, with some left over for fun and social occasions. You could holiday in the UK, eat out about once a month and do some affordable leisure activities about twice a week.

-

A ‘moderate’ lifestyle provides more financial security and more flexibility. You could have one foreign holiday a year and eat out a few times a month. You’d have the opportunity to do more of the things you want to do.

-

A ‘comfortable’ lifestyle allows you to be more spontaneous with your money. You could have a subscription to a streaming service, regular beauty treatments and two foreign holidays a year.

About half of employees are projected to have an income between minimum and moderate, while one in six employees are projected to have an income between moderate and comfortable.

At Armstrong Watson Financial Planning & Wealth Management, we work with you to build your retirement plans and regularly review these so you know if you will remain on track. Where appropriate, we can also use cashflow forecasting to allow you to better understand your plans and arrangements to help you make informed decisions.

Subscribe to

Insight

INSIGHT is our quarterly financial magazine packed full of useful and topical articles on financial planning and tax matters affecting you.

Recent news stories

Armstrong Watson can help

Whether you need expert accounting, strategic business advisory, tax planning, or financial guidance, our experienced team is here to support your success. From sole traders to large enterprises, we provide tailored solutions to help you navigate complex financial challenges and achieve your goals. Get in touch today to discover how we can help your business thrive – call 0808 144 5575.