The pension annual allowance trap

The annual allowance is an important number in the pension world. It sets the maximum tax-efficient amount of total contributions in a tax year – from any source – that can be made to pension schemes for your benefit. If the allowance is exceeded, then any tax relief you receive on the excess is effectively clawed back by the annual allowance charge. However, the tax status of the benefits bought with the unrelieved contributions remains unchanged, meaning potentially that 75% is taxable when withdrawn.

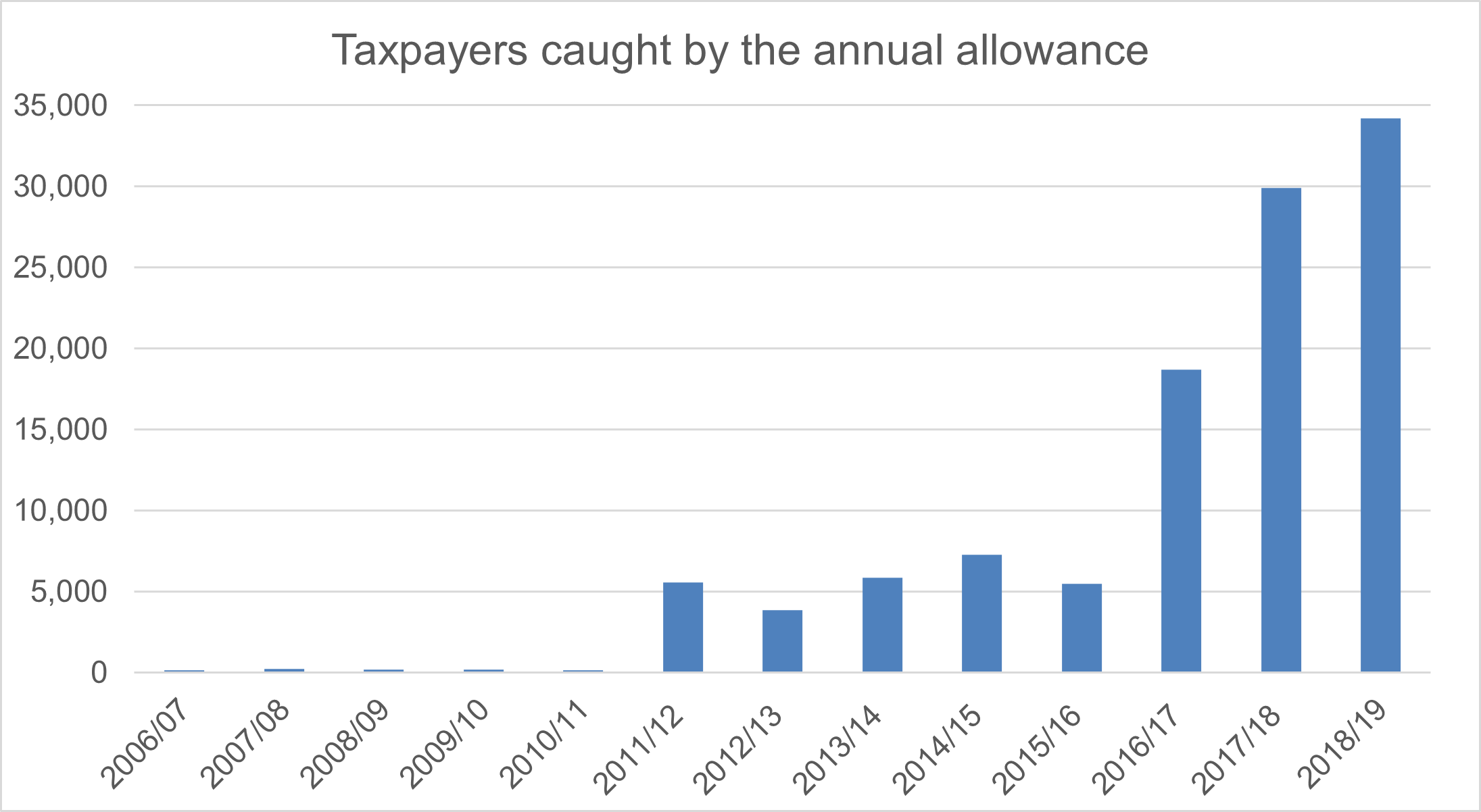

Until 2011, the annual allowance was set at a level that made it a somewhat academic topic – in 2010/11 it stood at £255,000. Then in 2011/12, it was reduced to £50,000 – a cut of about 80%. The Chancellor’s aim was to lower the cost of tax relief at a time when the top rate of income tax was 50%. Three years later, from 2014/15, there was another reduction to £40,000. In 2016/17 the axe fell for a third time but on this occasion, it was more a salami-slicing than a chop. The main allowance remained at £40,000 but it became subject to a taper that could bring it down to as little as £10,000 for high-income earners. It has fallen even further to £4,000 now.

Source: HMRC.

The effects of these changes are visible in the graph and show that annual allowance continues to help fill HMRC’s depleted coffers.

In 2010/11, only 140 people reported a liability for the annual allowance charge on their tax returns. That jumped to 5,570 the following year and 18,870 in 2016/17. At last count – three tax years ago – more than 34,000 people were caught with total excess contributions of £817 million. The vast bulk of that excess would have been taxed at 40% or 45%, netting perhaps £350 million for the Treasury.

The Chancellor was forced to relax the rules for tapering in the 2020 Budget because potential tax bills were prompting NHS consultants and other senior public sector staff to take early retirement or limit their working hours. The revised tapered annual allowance applied for individuals with “threshold income” of more than £200,000 and "adjusted income" of more than £240,000.

It is important to know the change in limits when looking to work out carry forward contributions from 2020/21 onwards as the calculation of any unused annual allowance from tax years prior to this is done using the old limits.

While the change should have reduced those paying the annual allowance charge in 2020/21, the problems it causes have not disappeared.

What is measured against the annual allowance?

The pension input amounts for all of a member’s pension arrangements will be tested against their annual allowance limit.

The pension input amount is dependent on the type of pension scheme:

- For a defined contribution (money purchase) scheme – all tax-relieved contributions paid by or on behalf of an individual, plus any employer contributions paid in respect of the individual.

- For a defined benefit or cash balance pension scheme – increases in the capital value of pension and tax-free cash retirement benefits (excluding death in service rights).

If you exceed the annual allowance

If you exceed the annual allowance in a particular tax year, you won’t get tax relief on any contributions you paid that exceed the limit in that tax year and you will be faced with an annual allowance charge.

The amount that exceeds the annual allowance by will be added to the rest of your taxable income for the tax year and be subject to Income Tax at the rate that applies to you.

You might be able to ask your pension scheme to pay the charge from your pension. This is known as Scheme Pays and means your pension would be reduced. This is not always possible so you do need to check with your pension provider first.

As you can see the rules around the annual allowance are complicated. If you think you might be getting close to your annual allowance, or you might have exceeded it, we strongly advise you to seek advice from a regulated independent financial adviser.

At Armstrong Watson, we are Chartered Independent Financial Advisers. We can help you understand how much your annual allowance is, including any unused amounts, whether you've exceeded your annual allowance, if there may be options to reduce any potential charge and look at your options for paying any tax charge that may be due.

Subscribe to

Insight

INSIGHT is our quarterly financial magazine packed full of useful and topical articles on financial planning and tax matters affecting you.

Recent news stories

Armstrong Watson can help

Whether you need expert accounting, strategic business advisory, tax planning, or financial guidance, our experienced team is here to support your success. From sole traders to large enterprises, we provide tailored solutions to help you navigate complex financial challenges and achieve your goals. Get in touch today to discover how we can help your business thrive – call 0808 144 5575.