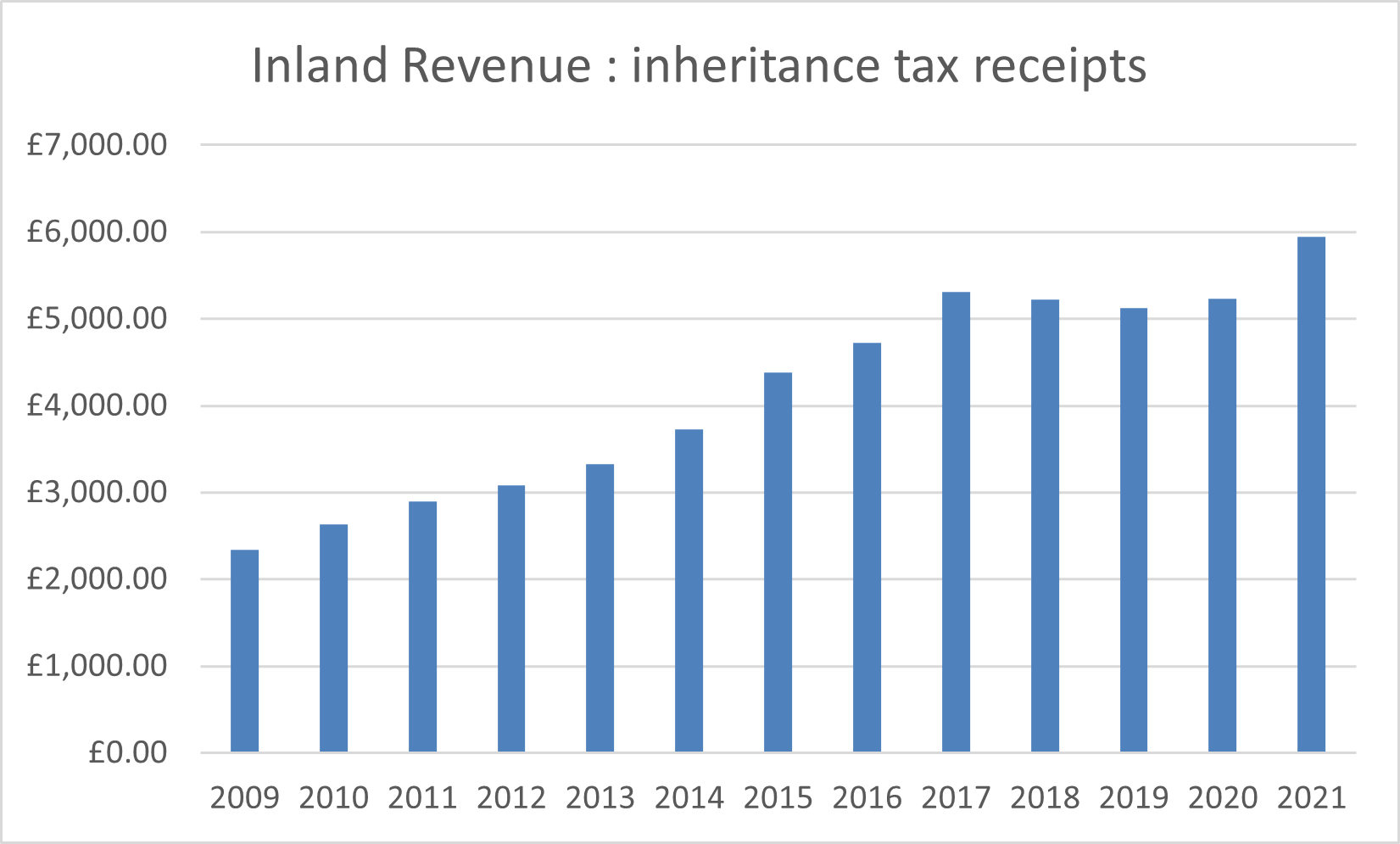

If you thought inheritance tax was now simply for extremely wealthy people to worry about, think again. IHT receipts have increased as a share of GDP since 2009-10, mainly due to rises in asset prices. Residential property makes up the largest share of most estates and average house prices have risen by more than 40 per cent in that period. In 2022-23 The Office For Budget Responsibility (OBR) has forecast that IHT will raise £6.7 billion and could be £7.8 billion by 2027/28.

The Nil Rate Band will increase to help keep me out of IHT won’t it ?

The nil rate band is the threshold above which IHT is payable, however, it has now been frozen at £325,000 since 2010/11 and will now remain frozen until April 2026. The nil rate band initially increased to £325,000 way back in April 2009 and who would have thought it would remain at this level for 18 years? The Residence Nil Rate Band was introduced in April 2017 at £100,000 and increased three times to £175,000 but has also been frozen until 2026. As estate values, supported by increased property prices and/or investment returns, continue to rise we will clearly see yet more people caught by the IHT net over the coming years, unless they take legitimate steps to help mitigate this, through careful financial planning.

There are ways to mitigate IHT for your family

There are currently many ways, with careful financial planning, IHT can be reduced, offset or eradicated altogether. Potential considerations could involve simply giving your money away to reduce your estate such as lifetime gifts or through regular surplus income, using life assurance policies to protect any tax liabilities, through to setting up trusts to shelter your assets. Solutions do not, however, have to involve a reduction in your lifetime benefit of funds or assets, it is a case of determining what is the right solution for each individual and family.

At the very least make a will

Many people often procrastinate when it comes to writing a will. We would therefore encourage everyone to make a will as soon as possible. According to research by Canada Life 3 in 5 adults in the UK don’t have a will.

Making a will so you decide who gets what of your assets. If you don’t clarify your wishes in a will, the state will take over and distribute your estate according to a formula set out in the rules of intestacy. The results are not always what you would expect and can also potentially create unnecessary tax consequences.

What steps can I take?

For the majority of people there are a various approaches that can be taken to mitigate a future IHT liability. These range from making gifts (large or small), putting money in to trust or even insuring the IHT liability. Of course, you could choose to ignore it. If there is tax to pay later on so be it. On the other hand you could spend enough money so that nothing is left which may be more difficult said than done!

The rules, however, around IHT can be complex, and the amount of tax, and even the overall rate that will be paid, will depend on how your finances are structured during your lifetime, how you dispose of your assets and to whom you leave them. Seeking independent tax and financial advice can help you pass your assets to the people you want to benefit and potentially mitigate some or all of the IHT liability.

At Armstrong Watson our quest is to help our clients achieve prosperity, a secure future and peace of mind. We provide bespoke tax planning, financial planning and wealth management all under one roof. Please note, advice on IHT related matters could be provided by a mixture of both our financial planning and tax specialists.

For more information or advice on how you can save on Inheritance tax, get in touch with one of our financial planning team on 0808 144 5575 or email help@armstrongwatson.co.uk.