National Insurance & Income Tax Reductions

Basic Rate of Income Tax

As part of the Spring Statement in March 2022 it had initially been announced that the basic rate of income tax would be reduced from 20% to 19% from 6 April 2024. However, on 23 September 2022 the Government have now brought forward this reduction by one year.

As a result, the reduced rate of 19% basic rate income tax will now apply from 6 April 2023.

Please note this will apply to non-savings income such as employment, rental and pension income for individuals resident in England, Wales and Northern Ireland. It will not automatically apply to non-savings income arising on individuals living in Scotland. The Scottish Government will set its own rates of income tax.

The reduced rate of basic rate tax will apply to taxable savings income irrespective of where an individual resides.

Additional Rate of Tax

On 23 September 2022 the Government also announced the removal of the additional rate of income tax of 45% on income over £150,000 from 6 April 2023. As a result, the top rate of income tax will be 40% from 2023/24.

Again, please note that this applies to non-savings income for taxpayers in England, Wales and Northern Ireland, therefore, there the changes will not automatically apply to individuals living in Scotland.

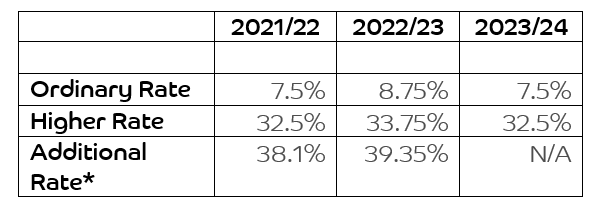

The dividend additional rate of 39.35% will also be removed to align with the dividend upper rate, which is being reduced to 32.5% from 6 April 2023.

Reversal of the Health and Social Care Levy

On 7 September 2021 the Government introduced plans to introduce a Health and Social Care levy in order to increase funding for the health and social care system. This was introduced from 6 April 2022 and initially increased Employer Class 1, employee Class 1, Class 1A, Class 1B and Class 4 National Insurance contributions by 1.25%. From 6 April 2023 the rates were due to return to their previous levels but a formal legal surcharge of 1.25% was to replace the increase in NICs rates and also apply to those working above State Pension age.

However, on 23 September 2022 the Government have now announced that the Health and Social Care Levy will be cancelled from 6 November 2022

Dividends

Dividends are not subject to NIC, therefore, the Government introduced separate measures to increase the rates of all dividend taxes by 1.25% from 6 April 2022.

This increase will remain in place for the duration of 2022/23 but will be reversed from 6 April 2023 as follows:

*Additional rate of income tax to be cancelled from 6 April 2023

Directors’ Loan Account

Whilst there has been no specific announcement with regards to tax rate applicable to overdrawn Directors’ Loan Accounts, the charge (commonly known as a s455 charge) follows the dividend higher rate tax charge. Therefore, this will remain at 33.75% for 2022/23 and will fall back to 32.5% from 6 April 2023.

Subscribe to

Inspired

Our monthly bulletin INSPIRED is packed with useful articles to keep you up to date with news and legislation that may affect you or your business.

Recent news stories

Armstrong Watson can help

Whether you need expert accounting, strategic business advisory, tax planning, or financial guidance, our experienced team is here to support your success. From sole traders to large enterprises, we provide tailored solutions to help you navigate complex financial challenges and achieve your goals. Get in touch today to discover how we can help your business thrive – call 0808 144 5575.