Cash interest rates are high, so why should you invest?

Over recent years investment markets have broadly performed below where we would expect them to do so over the long term. As a result, you may be questioning the value of your investments, particularly given interest rates on cash deposits are the highest they have been in well over a decade. Having experienced lower-than-average returns over recent years, you may be tempted to ask, ‘why bother?’

Historic conditions

Since 2016 we have seen an unusually volatile environment, with four major crises over this time, each causing periods of lost returns. The Brexit referendum in 2016, the US-China trade war of 2018, the pandemic of 2020, and the surge in inflation starting in 2022 which is still impacting markets to this day.

These events led to losses across wider markets, and while recoveries were experienced after the first three events, the periods of lost returns did significantly hamper investment performance over this period. What’s more, while markets staged an initial recovery following the inflation-induced losses of 2022, much of this has been lost as inflation proved overly stubborn throughout most of 2023. Sentiment is likely to improve once inflation subsides on a sustained basis, but for now, this remains a challenging time. While markets will always experience periods of growth and losses, and future crises will no doubt occur, the past few years have been particularly busy in this regard.

Economic and market outlook improving

Looking ahead, markets now appear to be in an improved position. While the threat of recession remains a possibility, economic conditions are much stronger than were previously expected.

Inflation is likely to continue falling over the coming months, and while there are question marks over the pace of these falls, the direction of travel looks clear. In this situation, interest rates appear at, or very close to, their peaks, and slow reductions are expected to begin during 2024. This means that businesses can plan for the future with more certainty, and a gradual recovery is expected from the current economic malaise. In the absence of any further market moving large scale macroeconomic shocks, future growth rates should therefore be improved.

At the time of writing (early December 2023) the situation in Israel and Gaza has the potential to develop into a market-moving shock, but currently appears unlikely to do so. There are huge levels of suffering and loss of life, yet the financial impact outside of the region has been limited and therefore markets, while wary, have not yet experienced large movements as a result of what is a truly horrible situation.

Beyond this conflict, markets continue to be preoccupied with the path of inflation and that of interest rates. 2022 saw large investment losses as markets expected higher rates to lead to recession, 2023 was broadly a static year as markets waited for inflation and interest rates to fade and this will likely continue over the coming months. A turning point for market sentiment is likely to occur when inflation falls to the level where central banks (and particularly the US Federal Reserve) are seen to be finished raising interest rates and are approaching the time to cut them. It is not possible to put a precise timescale on this, yet as the lagged impact of interest rates continues to take hold and the economy slows, the interest rate cycle will eventually turn, and at this point, a rally across most asset classes appears a strong possibility.

Potential turning point – recent inflation and interest rate developments

It cannot yet be said with confidence that the turning point has been reached, however recent developments suggest it is getting closer. Both the Bank of England and the US Federal Reserve opted not to raise interest rates further at their meetings in early November and markets rallied significantly. What’s more, markets have gained when inflation figures have come in at lower than expected levels in recent months. “One swallow doesn’t make a summer,” so it is important to note that these are just a few encouraging data releases and less positive news may well return, but it suggests a turning point is approaching, and importantly, it provides a strong hint to the direction which could be taken when inflation is eventually brought under control.

The last few years have been challenging for investment markets, but with inflation the most problematic it has been since the early 1980s there has been justified reason for this. Once this inflationary period fades, recovery for investment markets seems likely. Therefore, in the investment portfolios we manage at Future Money, we are acting with patience, positioned in those areas that are stable currently and which we expect to benefit from an uptick in wider market sentiment. In the meantime, bonds are now yielding their highest incomes in around 15 years and dividend rates on equities are attractive, and so the portfolios will benefit from these income streams. In addition, valuations across equity markets are broadly fair or good value (with the exception of some US technology stocks). As such, once inflation and interest rates do moderate, we expect capital values to perform well and patience to be rewarded.

Cash

At a headline level, cash appears the most attractive it has been since before the global financial crisis, particularly as other asset classes haven’t been performing any better over recent years, yet, at Future Money, we would argue it is worth considering this more closely.

If inflation continues to fall over the coming months and years as it is expected to, then interest rates would likely fall as well, which is important for two reasons. First, the return banks pay on cash deposits will be reduced, and second, as inflation and interest rates come down, we expect both equity and bond markets to rally. This means there is the potential for significant reinvestment risk; should markets strengthen over the next few years, investors who moved to cash and subsequently wish to return to the markets would be forced to buy in at higher levels. Of course, the opposite is also true if markets fall from here, and there are no guarantees on improved market conditions. Yet, given where valuations currently are, should sentiment improve (as inflation recedes), higher returns in market-based investments than in cash deposits would appear likely.

Cash investments are used in the Future Money portfolios, and we have the ability to have large allocations here, but currently we are not making full use of this allowance, with only small amounts held in cash. Allocations are instead focused in equity and bond markets, which we expect to outperform over the medium term, albeit with higher levels of volatility than will be available with a purely cash-based strategy.

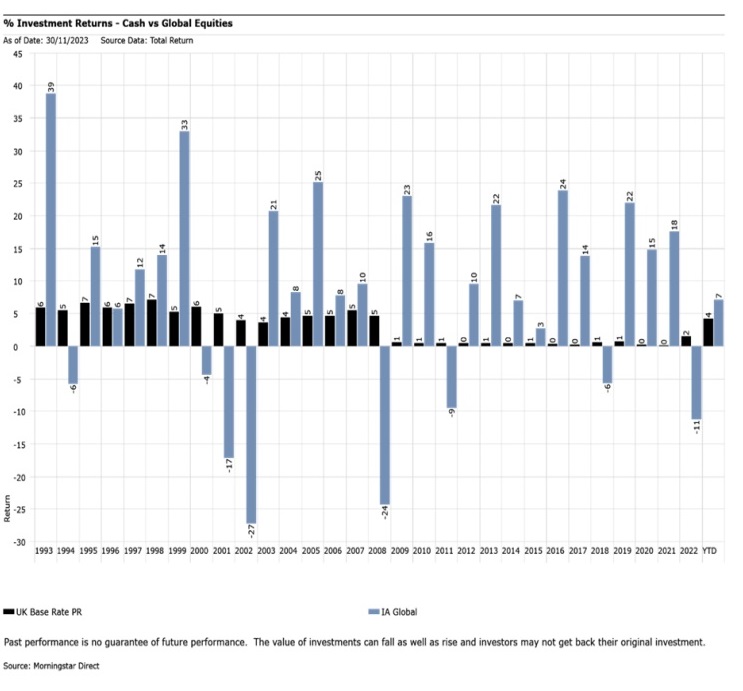

Performance – a long-term perspective

Interest rates are the highest they have been since 2008 and given recent volatility, investment markets have been far from inspiring. Here I’ve suggested that to lose faith now may be misjudged, but what has happened historically, particularly in times when interest rates were higher?

The chart below shows the returns achieved by cash deposits (UK Base Rate) and by global equities (as represented by the Investment Association’s Global sector average) over the past 30 years, and in 2023 to the time of writing (YTD: 1st Jan ’23 – 30th Nov ’23).

Of those 30 full years, while cash has outperformed in nine years, global equities have outperformed 21 times, 70% of the time.

The past is no guarantee of the future, yet this shows that even when interest rates have been high, an investor would typically have experienced greater returns having been positioned in equities.

This is a simplification of the argument, with bonds making up a significant part of many portfolios. Yet, the point is included to illustrate that while volatility must be endured and weaker periods do occur, investors who seek growth over the long term would be wise to properly consider the path that markets may take in the future.

Important Information

Please note that the contents are based on the author’s opinion and are not intended as investment advice. Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise and investors may get back less than they invested.

Subscribe to

Insight

INSIGHT is our quarterly financial magazine packed full of useful and topical articles on financial planning and tax matters affecting you.

Armstrong Watson can help

Whether you need expert accounting, strategic business advisory, tax planning, or financial guidance, our experienced team is here to support your success. From sole traders to large enterprises, we provide tailored solutions to help you navigate complex financial challenges and achieve your goals. Get in touch today to discover how we can help your business thrive – call 0808 144 5575.