Law firm benchmarking review 2024/2025 provides positive findings

By Victoria Lovell, Legal Sector Manager

As part of our annual accounts and tax compliance service, we provide all of our law firm clients with a bespoke benchmarking report for their practice, which analyses their financial performance for the year and compares it with similar firms. It forms a core element of our added value offering, and clients consistently find it extremely helpful when reviewing their annual accounts.

Each year, we also produce an annual benchmarking review summarising the results of all participating firms across the UK. Where possible, the findings are broken down by practice size. Practice size is defined by the number of full equity partners, excluding fixed share and salaried partners. Firms with 1–7 full equity partners are classified as small, while those with 8 or more are considered large. In practice, firms with 8+ full equity partners sit at the upper end of the legal market, reflecting the sector’s overall demographics.

This article summarises the results from our 2024/25 benchmarking review, mostly based on firms with year ends to March or April 2025. We have seen the following key trends:

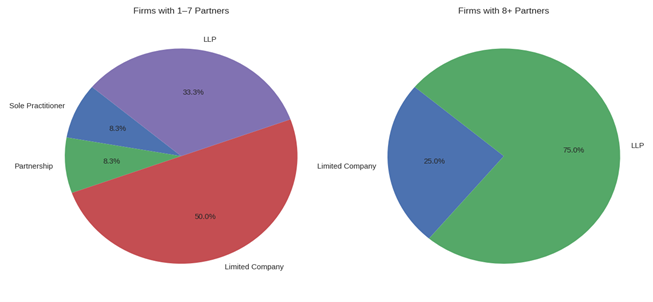

Firm structure

The structure of firms continues to vary due to size. Larger firms continue to be a mixture of LLPs and limited companies. Smaller firms in the majority are limited companies, with the number of LLPs rising and traditional partnerships and sole practitioners still existing to a smaller extent.

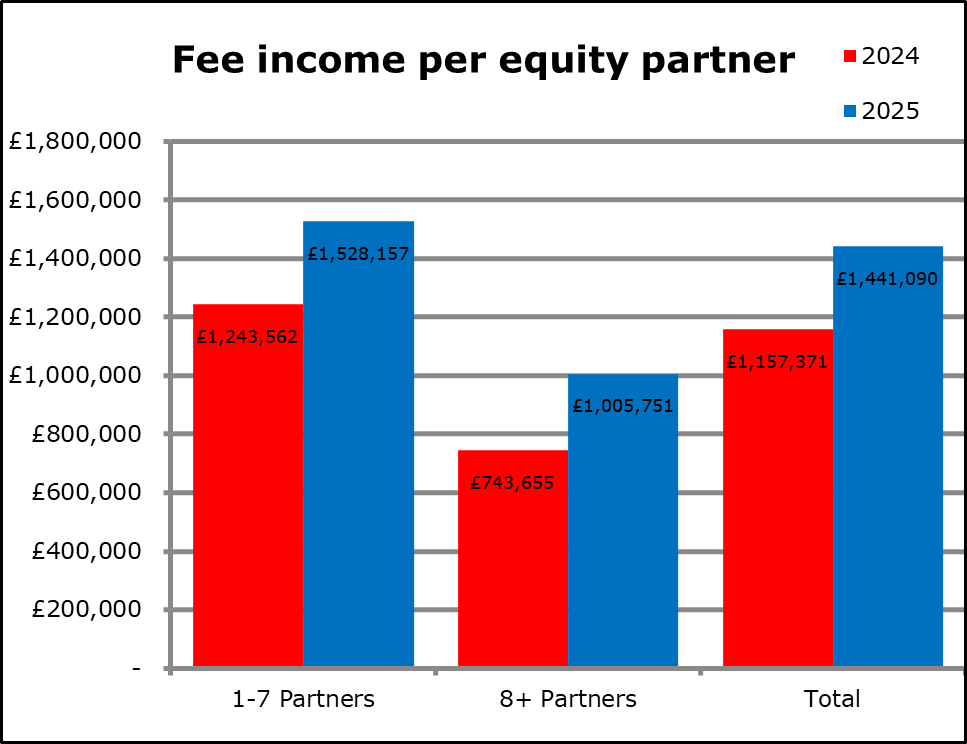

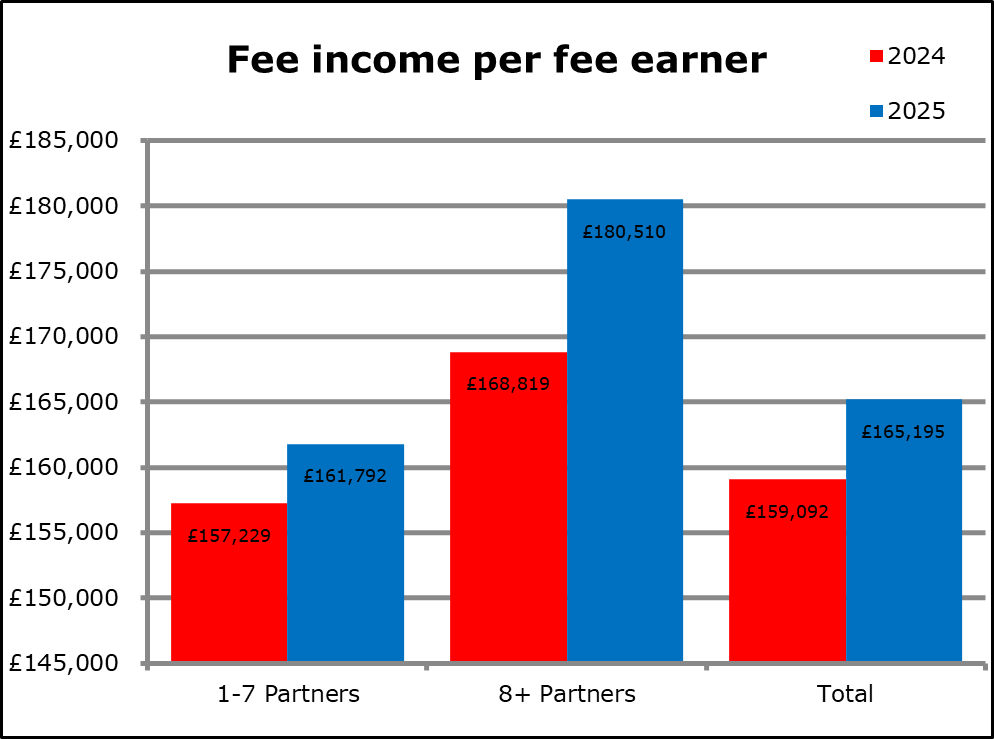

Fee income

Fee income per equity partner has risen by 25% since 2023/24, bringing the current average to £1.4m. The strongest growth has come from larger firms, where average fee income per equity partner has increased 35% to £1m in 2024/25, up from £744k in 2023/24. This compares with a more modest, but still impressive, 23% increase among firms with 1–7 partners taking the average up to £1.5m. Fee income per fee earner has remained broadly in line with the previous year, averaging £165k in 2024/25 compared with £159k in 2023/24.

Net profit

Average net profit (NP) per equity partner has risen modestly to £300k, up from £290k in 2023/24. Across firm sizes, net profit per equity partner stands at £295k for 1-7 partner firms and £329k for 8+ partner firms. Larger firms have seen a 13% increase compared with 2023/24, while smaller firms have recorded only a 2% uplift. Notably, both groups reported similar profit per equity partner levels last year (£289k for 1-7 partner firms and £293k for 8+ firms), making this year’s divergence more pronounced.

Net profit percentage (NP%) has dipped slightly overall, falling from 32.8% in 2023/24 to 27.7% in 2024/25. This decline is driven primarily by smaller firms, where NP% has dropped to 27% from 31.4%. Larger firms, by contrast, have maintained a higher NP% of 31.2%.

The net profits of smaller firms have been impacted by recent falling interest rates. In the previous year, higher interest rates boosted firms' temporary income, with interest received sometimes accounting for 10-15% of net profit. The fall in the base rate has compressed this figure, reducing interest income to 5-10% of net profit, but it is clear that many smaller firms are still reliant on client account interest for the profits being distributed to partners.

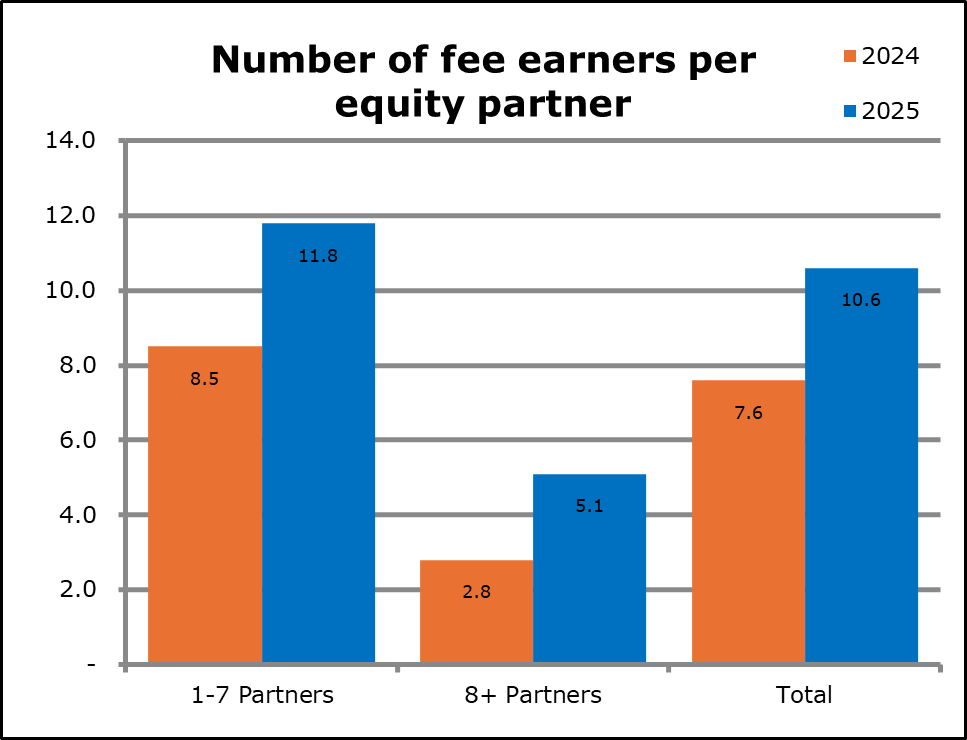

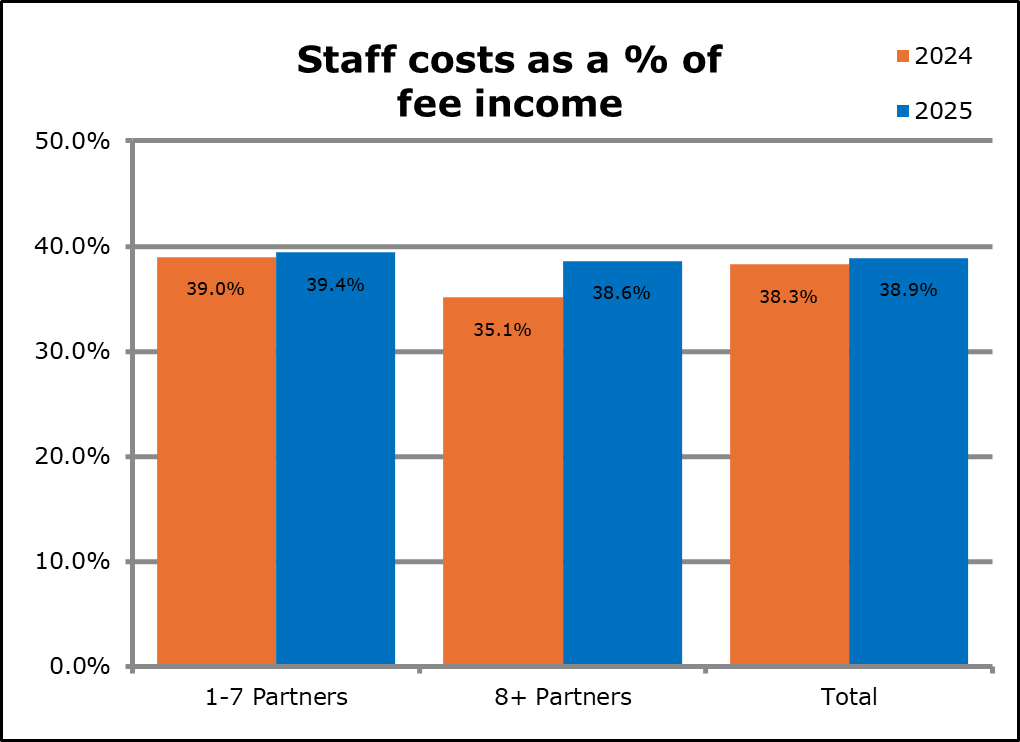

People

In 2024/25, firms have an average of 10.6 fee earners for every equity partner, up from 7.6 in 2023/24. However, this increase in ratios is primarily from reduction in equity partners rather than significant increase in fee earning staff numbers.

Overall staff costs as a percentage of fee income have risen slightly, increasing from 38.3% in 2023/24 to 38.9% across all firms in 2024/25. Smaller firms have seen staff cost ratios increase from 39% to 39.4%, while larger firms have experienced a more significant rise, from 35.1% to 38.6% over the same period.

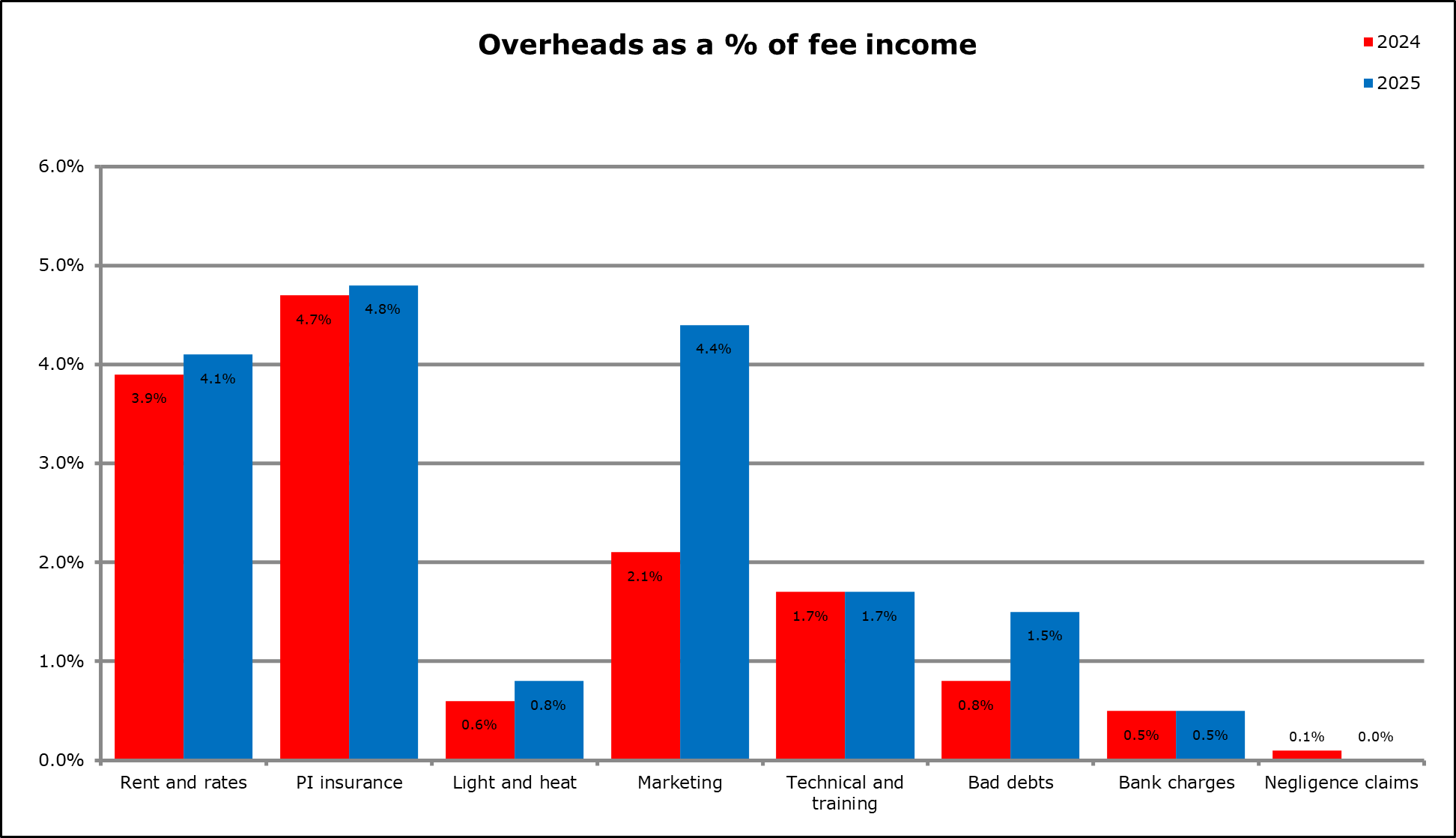

Overheads

Rent and rates have risen slightly in 2024/25, increasing from 3.9% to 4.1% of fee income. PI insurance has also edged up, moving from 4.7% in 2023/24 to 4.8% in 2024/25. As in previous years, the gap between smaller and larger firms continues to widen: PI costs for small firms now average 5.1% of fee income, compared with just 3.4% for larger firms.

The most notable increase in overheads for 2024/25 relates to marketing expenditure. Marketing costs have more than doubled as a percentage of fee income, rising from 2.1% in 2023/24 to 4.4% in 2024/25. This shift is driven largely by smaller firms, where marketing now accounts for an average of 5% of fee income. The increase reflects a move away from traditional advertising methods, with smaller firms in particular investing more heavily in digital marketing and the use of AI.

Summary

The findings from our latest benchmarking review remain very positive, with both smaller and larger firms demonstrating strong performance, particularly in terms of fee income. Larger firms continue to deliver solid profit levels, while smaller firms are beginning to feel the impact of falling interest rates, which had previously bolstered their results.

Subscribe to

Inspired

Our monthly bulletin INSPIRED is packed with useful articles to keep you up to date with news and legislation that may affect you or your business.

Related news stories

Armstrong Watson can help

If you are interested in discussing how your firm compares with the benchmarks in this report or you would like to discuss your firm’s performance, please get in touch. Call 0808 144 5575 or email help@armstrongwatson.co.uk.