Many people question why they are effectively being taxed twice on their assets. Firstly whilst building them via their earnings throughout their working lives, and then again when they die.

IHT was initially introduced on the idea of redistributing wealth for the benefit of the general public. The principle being, rather than the rich getting exponentially richer through large inheritances, a portion of their wealth is redistributed to the public through taxation.

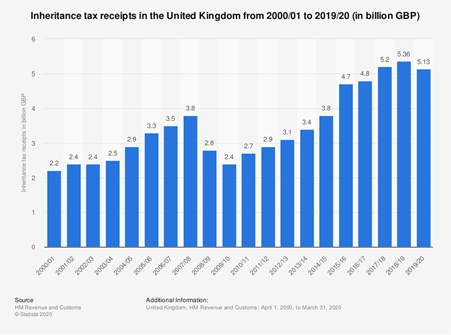

However, if you thought IHT was just for extremely wealthy people to worry about, think again. Rising property prices in particular means that inheritance tax receipts paid to the Exchequer continue to rise. HMRC collected £5.13 Billion in IHT in 2019-20 and the amount of inheritance tax collected in the future is currently expected to reach £6.3 billion by 2023-24.

In an attempt to alleviate the burden of IHT on increasing property prices in particular, a number of years ago now the Conservative Government introduced an additional allowance called the Residence Nil Rate Band (RNRB) in addition to the Nil Rate Band (the standard estate threshold). This now means a married couple or civil partners can pass up to £1 Million on to their heirs, rather than the previous £650,000 (the £325,000 Nil Rate Band x 2). However, this measure appears to have only temporarily reduced the IHT tax taken, as can be seen in the graph above, and without further favourable changes, as commented on earlier, is likely to increase further over the coming years.

Thinking about how your assets will be distributed after your death is not always a comfortable thought, however, it is one of the most important and valuable things you can do. At the very least you should make a will so you decide who gets what of your assets. If you don’t clarify your wishes in a will, the state will take over and distribute your estate according to a formula set out in the rules of intestacy. The results are not always what you would expect and can also potentially create unnecessary tax consequences.

The global pandemic and the unprecedented recent borrowing by The Government means that all taxes, allowances and reliefs both now and in the future are likely to be under closer scrutiny. One such area is likely to be that of IHT. In fact, over two years ago now, independent reports were commissioned by the then Chancellor, Philip Hammond, from the Office of Tax Simplification(OTS) on simplifying the IHT regime. The OTS have issued two reports to date, but no action has yet been taken in any subsequent Budgets. A Chancellor with an eye towards a ‘levelling-up’ agenda and a need for more revenue could finally decide to act in either the coming or future Budgets.

There are currently many ways IHT can be reduced, offset or eradicated altogether. Potential considerations could involve simply giving your money away to reduce your estate such as lifetime gifts or through regular surplus income, using life assurance policies to protect any tax liabilities, through to setting up trusts to shelter your assets. Solutions do not, however, have to involve a reduction in your lifetime benefit of funds or assets, it is a case of determining what is the right solution for each individual and family.

The rules around IHT can be complex, and the amount of tax, and even the overall rate that will be paid, will depend on how your finances are structured during your lifetime, how you dispose of your assets and to whom you leave them. Seeking independent tax and financial advice can help you pass your assets to the people you want to benefit and potentially mitigate some or all of the IHT liability. With the right planning and support some of the IHT receipts currently payable by individuals are thereby able to be legitimately avoided or reduced.

At Armstrong Watson, our quest is to help our clients achieve prosperity, a secure future and peace of mind. We are able to provide bespoke tax planning, financial planning and wealth management all under one roof to help ensure that our clients have the best opportunity to pass on their wealth to those they wish to receive it.

For advice on inheritance tax, get in touch with Simon Mayoh on 07860 846370 or email simon.mayoh@armstrongwatson.co.uk