Inheritance Tax: Business Property Relief Important Changes

There has been much media attention on the impact of proposed Inheritance Tax (IHT) changes on the farming community but it is important to emphasise that these changes will affect not only farmers, but all businesses including sole traders, partnerships and companies.

Like Agricultural Property Relief (APR), Business Property Relief (BPR) has largely allowed businesses to pass down families tax-free on an owner’s death. For that reason, business owners have been less concerned about mitigating Inheritance Tax (IHT) on BPR assets. However, the rules are due to change from 6 April 2026, and many businesses will need to prepare or review their succession plans.

What is BPR?

Simplistically, BPR reduces the value of qualifying business property chargeable to IHT. BPR is allowed at:

- 100% for assets including unincorporated businesses, an interest in a business (e.g., sole traders, partnerships or unquoted shares), or shares listed on an alternative stock exchange (e.g., AIM); or

- 50% for assets including land/buildings/equipment used in a business but owned personally by the business owner.

What’s changing from 6 April 2026?

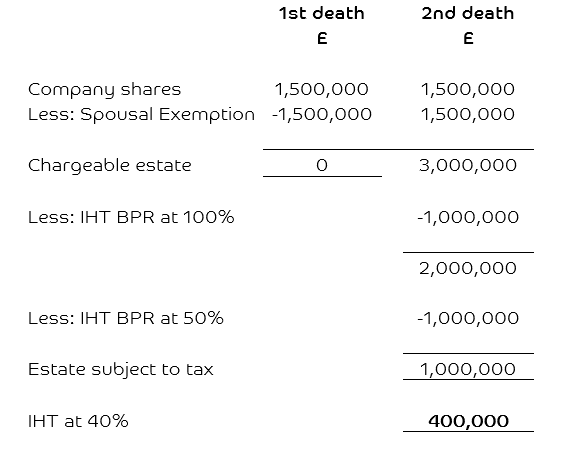

Under the proposed changes, owners of private trading companies and/or partners in trading businesses will only have a combined £1 million allowance for assets which qualify for 100% BPR and 100% APR. Above that, relief will be restricted to 50%. Essentially, this means that a rate of 20% will be charged on qualifying assets over £1 million. The example below illustrates the potential impact of the changes and how an owner of a qualifying business worth £3 million could now face an IHT bill of £400,000.

Like the IHT Nil Rate Band, the £1 million allowance will refresh every seven years on a rolling basis, so gifting could potentially be repeated over time. However, the legal and tax consequences of doing so must first be understood.

The allowance (or any unused part of it) cannot be transferred to a surviving spouse or civil partner. Some individuals might, therefore, wish to rewrite their wills to ensure that any unused allowance is not wasted (e.g., by possibly leaving assets to others or putting them into trust).

Opportunities to transfer BPR/APR assets into trust exist, but the Government is considering rules to prevent individuals from reducing their total IHT exposure by transferring qualifying assets to more than one trust (i.e., there is likely to be be one £1million allowance not a £1 million allowance per trust). These rules must be borne in mind when drawing up any plans involving trusts.

Example - impact of changes to BPR

This example is purely for illustrative purposes. It ignores any available IHT Nil Rate Bands and other assets and assumes that: -

- A married couple hold shares equally in their qualifying family business

- The business is valued at £3 million

- On the first death, the shares are transferred to the surviving spouse

If both individuals die before 6 April 2026, there will be no IHT liability (as 100% BPR would be available).

However, if they die on/after 6 April 2026, the potential IHT liability will be: -

Important issues and potential risks

Lifetime gifts and/or the transfer of property into trusts could be advantageous, but care is needed, particularly where the owner retains a benefit in the property.

Likewise, the potential risks of dividing assets need to be considered alongside the benefits of keeping the assets under single ownership.

Specialist valuation advice will also be required to confirm the tax liability (or otherwise) on lifetime gifts or transfers into trust. Previously, this was rarely needed as no tax was at stake.

Can IHT be mitigated?

BPR remains valuable - it reduces the IHT rate on qualifying assets over £1 million from 40% to 20% - so all business owners should fully review their affairs to maximise this important relief. Steps can be taken before 6 April 2026 to further reduce the tax exposure and preserve wealth but careful planning and professional advice are key to securing the best possible results. In advance of the final legislation, now is the best time to start exploring options.

Subscribe to

Agri Matters

Agri Matters is our quarterly online newsletter that provides you with the latest financial information and legislation updates affecting British farming businesses.

Armstrong Watson can help

Whether you need expert accounting, strategic business advisory, tax planning, or financial guidance, our experienced team is here to support your success. From sole traders to large enterprises, we provide tailored solutions to help you navigate complex financial challenges and achieve your goals. Get in touch today to discover how we can help your business thrive – call 0808 144 5575.