The importance of pension planning for young people

Most retirees are in receipt of pensions - whether this is via drawdown or annuities – and nearly everyone will find themselves relying on monies set aside in their earlier working lives to support them in retirement.

For this reason, pensions are just as important - perhaps even more so - to young people as they are to those approaching retirement.

Don’t rely solely on your State Pension

While many believe the State Pension will support them in retirement, it falls short of average salaries and the expected level of income needed in retirement.

The current State Pension (12.09.24) is £221.20 per week – or £11,502 per annum. Comparatively, the average salary for those in their 20s in the UK is £30,316. The question to ask here is: could you afford to live without the £20,000 per annum?

It's expected that a single person will need £14,400 per year for a minimum standard of living in retirement, according to the Pension and Lifetime Savings Association’s Retirement Living Standards (PSLA). For moderate standard of living the expected retirement income needed is £31,300, while for a comfortable standard of living PLSA suggests £43,100 would be required.

As such, placing as much into a pension as early as possible can be a great way of saving more effectively for retirement, to ensure you meet your future goals.

Employer pension contributions

The total minimum contribution for a workplace pension is 8%, with your employer contributing a minimum of 3% of your salary. You also make a personal contribution, which is taken from you salary before tax. You can choose to increase you contributions and some employers may match your payments, effectively doubling your pension contributions.

Therefore by remaining in your workplace scheme, not only are you saving for retirement, but your employer is also adding to your pension pot.

But did you know that you can also get extra money on top of your personal contributions?

Pension tax relief

Every personal contribution placed into a pension attracts basic rate tax relief. This means that for a UK basic rate tax payer, every personal contribution of £100, you receive an extra £25 within the pension wrapper. There’s few opportunities where money is free, but pension contributions are one.

£25 may not seem much, but regular contributions can soon add up. Across a full year, £25 per month tax relief is £300 extra added to your pension.

For higher and additional rate taxpayer, higher rate and additional rate relief is applied by extension of your basic and higher rate bands which could result in a tax reclaim or a tax code adjustment.

Compound interest and growth

Investing as early as possible is helped by compound growth.

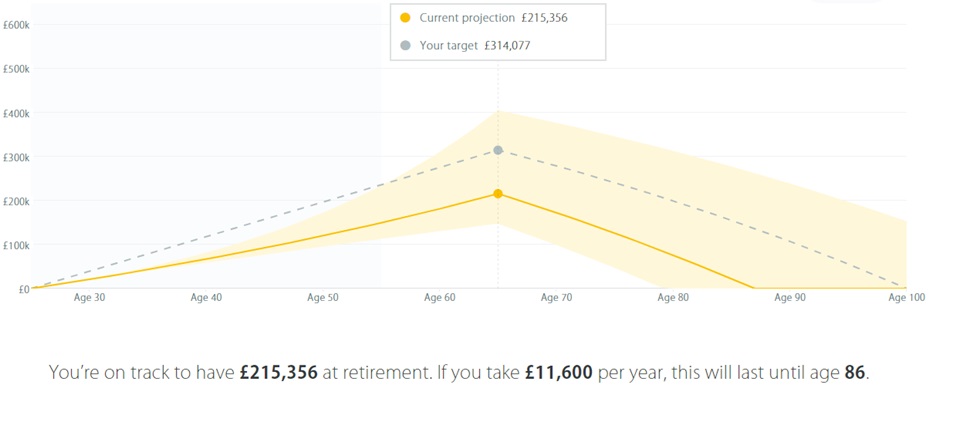

As an example, Ms Armstrong puts £150 personal contribution in her pension pot every month (which is matched by her employer) from age 25 to 65. Assuming compound growth of 5% year on year, this could achieve a fund value of approximately £215,356 by the time she retires – a total percentage return of 49.55%.

In comparison, Mr Watson pays in the same from age 40 to 65 and could achieve a fund value of £119,709 – a return of 33.01%. Therefore not only has he put less money into his fund by delaying pension planning, but the fund has grown by less over time as a result.

Source: PensionBee Pension Calculator

Key things to consider

While it is true that we must balance future plans with the here and now, pension planning should be fundamental to any young person’s holistic financial plan.

Key tips for cashflow:

- Prioritise committed expenditure (rent/mortgage, bills, food, etc).

- Have separate pots of money - emergency fund, savings, pension.

- Anything surplus should be considered for pension purposes.

Subscribe to

Inspired

Our monthly bulletin INSPIRED is packed with useful articles to keep you up to date with news and legislation that may affect you or your business.

Related news stories

Recent news stories

Armstrong Watson can help

Whether you need expert accounting, strategic business advisory, tax planning, or financial guidance, our experienced team is here to support your success. From sole traders to large enterprises, we provide tailored solutions to help you navigate complex financial challenges and achieve your goals. Get in touch today to discover how we can help your business thrive – call 0808 144 5575.